Over the past two decades, corporations have doubled their profits but contributed increasingly less to state revenues. Where is all the money going?

(Shutterstock)

(Shutterstock)

When Rick Snyder became governor of Michigan in 2011, his state had been on a 10-year economic slide -- businesses were leaving and so were people. Where the rest of the country saw growth in the first two-thirds of the 2000s, Michigan’s fiscal health was slip-sliding away.

Reversing a slide is difficult, and Michigan’s governor and legislators focused a good chunk of their turnaround efforts on taxes. They wanted to reform the tax code so that it would lure businesses and generate the revenue needed to underwrite the kind of quality services that make people want to live there. Snyder’s first step was to ask the legislature to slash business taxes. Within months, lawmakers repealed the unpopular and complicated Michigan Business Tax -- though businesses could opt to stay with parts of the old system and its arcane web of credits and rebates. That isn’t all the legislation did. The new tax law created a flat 6 percent tax that only certain types of corporations paid on their income. Talk about simplification: Nearly 100,000 businesses no longer had to file corporate returns.

Michigan has made economic progress since the 2011 tax reforms were passed. The population has stabilized, and the state ranks fifth in the country in job creation. Earlier this year, Michigan’s bond rating was upgraded, an affirmation of a more stable fiscal environment.

But tax policy changes don’t happen in a vacuum. It’s difficult to tell whether the state’s upturn is a result of the national economy recovering from the 2008 recession or from changes to Michigan’s business taxes. What is certain, however, is that the tax reform is bringing in less money. Before the 2008 recession, Michigan was collecting more than $2 billion annually in business taxes; in 2013, collections were less than $1 billion. That fall-off is in keeping with an in-state trend that had been building for two decades: Michigan corporate tax collections, adjusted for inflation, have fallen by 72 percent. Meanwhile, perhaps counterintuitively, total state revenues over that period grew by 56 percent.

Michigan is just one of a handful of states that has seen corporate tax revenue drop sharply, but it is one of many that has watched that tax base shrink while overall tax revenue grows. Nationally, real net corporate income revenues have grown on average at about half the pace of total revenues in states collecting the taxes over the past two decades, according to a Governing analysis of financial data reported to the U.S. Census Bureau. This weak growth of corporate taxes took place despite rising corporate profits, which more than doubled in the same time period, according to the St. Louis Federal Reserve Bank.

State tax policy clearly played a role in the diminishment of corporate tax revenue. As Greg LeRoy notes in his book The Great American Jobs Scam, federal corporate income tax revenues grew annually by 6 percent in the second half of the 1990s; state corporate income tax revenues grew by just half that rate. “Same companies, same profits, same years -- half the tax,” says LeRoy, who is also executive director of Good Jobs First, which tracks corporate tax giveaways.

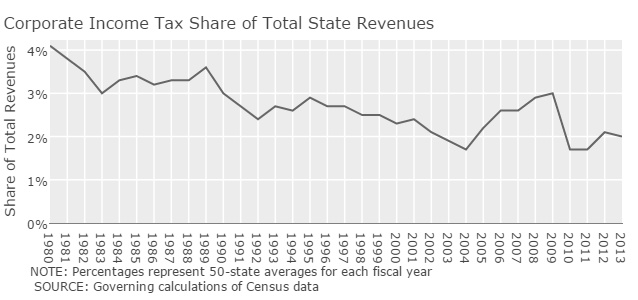

The bottom line for states is that over the past three years, corporate income tax has represented 1.9 percent of total annual revenues. That’s down significantly from an average of 2.7 percent over the decade of the 1990s and 3.5 percent over the decade of the 1980s.

Data by Mike Maciag

Data by Mike Maciag

Michigan’s corporate tax reforms required sacrifice, especially in the form of a revenue hit. The reforms called for the state to continue to pay out any remaining tax credits under the old system. In fact, the state gave out nearly as much in rebates as it received in corporate tax revenue in 2015, according to Michigan Treasury spokesman Terry Stanton. Over the next few years, however, those credits are expected to decline to $600 million annually. Stanton also notes proprietorships no longer subject to the old business tax are reporting their business earnings as personal income. About $900 million in income tax revenue this year is due to that shift.

The positive news for Michigan is that the downturn in corporate revenue is about to end. The 2011 reforms eliminated a number of loopholes and ended preferential treatment for some industries, such as tax credits to woo the filmmaking industry and to keep automobile manufacturers in the state. The state’s treasury office expects corporate tax revenue will total more than $1 billion this year and the next.

But critics of the 2011 tax program point out that Michigan now ranks near the bottom in corporate income tax revenue per capita among the states that levy such a tax, according to the Michigan League for Public Policy. The state paid for part of the corporate cuts by eliminating most individual income tax deductions and credits, and by partially taxing retiree incomes, which had been exempt. “We cut taxes on businesses by a lot, but in reality we just shifted it on to individuals under the guise of a simpler tax system,” says the policy league’s Rachel Richards.

While Michigan’s case is more extreme, most states have lackluster corporate revenue growth compared with other revenue streams. Colorado, however, is one of the 10 states where corporate income tax revenue has increased at a faster pace than total revenue. This may be due in part to several decades of economic growth. The state has added 2 million people since 1990, a population increase of 60 percent. Colorado has consistently ranked among the top states for business, not necessarily because of its business environment but because of its economic climate and educated labor force. “We’re very much on the cutting edge of the creative economy,” says Carol Hedges, executive director of the Colorado Fiscal Institute. “Increasingly, it’s about lifestyle -- those intangibles. People are flocking here.”

In short, there’s no cookie-cutter solution that can be applied from one state to the next to attract businesses, people and jobs. Business tax breaks are no panacea. Policymakers need to study economic trends in their region to understand what is actually helpful to companies, says Zach Schiller, executive director of Policy Matters Ohio. He points to one of Ohio’s recent gross receipts tax adjustments that allows sole proprietors to exempt some of their business income. Set up as an incentive for small businesses, the change nets small businesses just several hundred dollars, yet will cost the state hundreds of millions of dollars. “The idea that we’re doing small businesses a favor with this is ill-conceived,” he says. “It’s like flying an airplane over Ohio and throwing money out the window.”

When it comes to tax incentives, LeRoy would like to see states ask more of corporations in return for the tax favor. So-called community benefits agreements, for instance, often include local hiring requirements, job quality standards and affordable housing set-asides. A broad coalition of labor and community-based organizations negotiated such an agreement with the developers of Los Angeles’ downtown sports and entertainment complex in 2001.

Businesses that refuse to make any trade-offs should make lawmakers wary, LeRoy adds, pointing to a recent experience in Illinois. In 2013, the head of Decatur-based Archer Daniels Midland announced he wanted to relocate to Chicago but needed a tax credit to help pay for the cost -- otherwise he might have to move out of state. Legislators balked at the threat, called it blackmail and did nothing. In December of that year, Archer Daniels Midland announced where it had decided to open new offices: Chicago -- no incentives required.

The slashed business taxes, the incentives and assorted rebates that woo corporations aren’t the only reason corporate tax revenue is down. There is a growing sophistication in the ability of big corporations to shelter profits in offshore tax havens. The Institute on Taxation and Economic Policy (ITEP) estimates that Fortune 500 companies reporting profits pay an average of 3.5 percent in state corporate taxes. The average state corporate income tax rate, however, is about 6 percent nationwide.

The sheltering of profits got a boost from computerization, which made it easier for companies to move profits around on paper, notes ITEP’s Executive Director Matthew Gardner. He says states can close a key loophole in their corporate tax laws by requiring companies to report their income from overseas. This move -- known as combined reporting -- effectively treats a parent and its subsidiaries as one corporation for state tax purposes. About half the states have implemented combined reporting, which discourages companies from using noncorporate income tax states as tax havens. But few states expand that requirement to international holdings.

“Thirty years ago,” Gardner says, “the cutting edge in income shifting was moving profits to Delaware or Nevada [states that have significant tax advantages for corporations]. Now they’re shifting them out of the country entirely.”

Data compiled by Mike Maciag

Data compiled by Mike Maciag